Katharine Byrne, Head of Corporate Finance recently contributed to the latest edition of BDO Horizons to report of the recent M&A activity in the UK and Ireland.

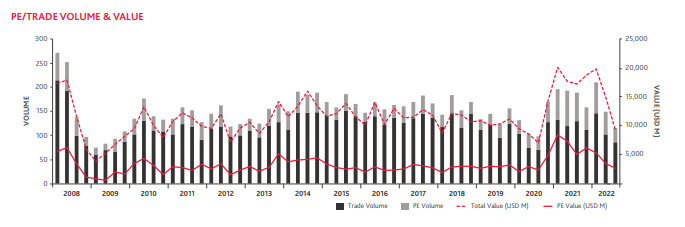

After record breaking levels of M&A activity in 2021, it was anticipated that 2022 would be another impressive year. With continued pent-up demand and excessive capital, dealmaking was forecast to maintain momentum. However, the invasion of Ukraine resulted in the M&A market becoming more volatile and fragile. Despite relatively steady first half to the year, the pace of overall mid-market M&A activity in UK and Ireland significantly slowed in Q3 2022 as companies assessed the impact of the war and soaring inflation. During the quarter there were 113 transactions reported with aggregate value of $9.1bn, down from 146 deals in Q2 and the lowest level of activity since the Covid crisis two years ago. While some additional transactions will be reported after date of writing, there is notable increase in number of transactions not disclosing deal consideration which is likely to be influenced by a reluctance to disclose valuations during these uncertain times.

The slowdown in deal activity is across both trade and financial buyers which is surprising given the level of dry powder available in the market. Private equity transactions dropped to 29 reported deals with aggregate value of $2.6bn, representing 26% of total activity. Trade volumes held steady at 84 deals, as corporates continue to consolidate their market positions through M&A. While the pressure is on Private Equity to deploy capital, in our experience transactions are taking longer as buyers take their time going through the due diligence process. Deal structures are also changing with higher number of earnouts and deferred consideration as buyers and sellers seek to bridge the gap in valuation expectations.

Key sectors and deals

In terms of sector activity, TMT remains the most active with 34 transactions reported during the quarter, representing 30% of all activity. TMT continues to increase in proportion to all activity representing 35% of year-to-date transactions, up from 32% in 2021 and 30% in 2020. This trend will continue with increasing number of TMT transactions, although the focus for tech companies has certainly shifted to generating profits rather than loss-making with potential for scale! AI, Cyber security and FinTech are all attracting high levels of investment. TMT represented five of the top 20 transactions during the quarter with deals such as The Access Group acquisition of Pay360 and the buyout of Sepura Limited by Epiris private equity.

Business Services was the next most active sector during the quarter with 18 deals (up from 16 in prior quarter). One of the notable transactions in this sector was Marks & Spencer’s acquisition of its logistic provider Gist for $305m in an effort to secure its supply chain. We are likely to see further consolidation across the logistics sector both in UK and Ireland as operators merge to achieve scale and extract synergies during these turbulent times.

The Industrial & Chemicals sector was also steady with 15 reported transactions followed by Financial Services with 14 deals, no change from prior quarter.

During the last quarter, the top 20 transactions totalled $5.5bn, representing nearly 60% of total reported values in the mid-market. There is still strong inbound activity with seven of the buyers from US, three of which were in the pharma and healthcare space; Arcutis Biotherapeutics acquisition of Ducentis BioTherapeutics Ltd for $430m, Gilead Sciences acquisition of MiroBio Ltd for $405m and the $160m investment by Kairos HQ into Cera Care.

As the UK navigates through the current political crisis, we are likely to see increase in distressed transactions as Covid-related government supports are withdrawn and opportunistic buyers’ avail of weakening currency and lower valuations. Ireland’s outlook is more positive with strong economic indicators and continued foreign direct investment across the Tech, Financial Services and Life-Science sectors.

Looking ahead

The final quarter of 2022 is likely to see subdued levels of midmarket M&A as companies grapple with challenges of rising inflation, supply chain disruption and talent shortage. According to the BDO Heat Chart there still is strong appetite for deals in the UK & Ireland with 540 rumoured deals, although some of these transactions may be postponed until 2023. TMT is predicted to continue to be the dominant sector with 117 deals, followed by Industrials & Chemicals (86) and Consumer (81). Inflationary growth, the cost-of-living crisis and weaker consumer confidence combined with higher borrowing costs will all be at forefront of deal-makers minds when considering whether timing is right for M&A.

Content adapted from BDO Horizons 2022 – Issue 4.