The European Commission’s Omnibus proposal represents a major milestone in the evolution of the European Union's (EU) sustainability regulation. The initiative aims to simplify reporting, reduce administrative burden and boost European competitiveness while ensuring the long-term integrity of the EU’s sustainability framework.

On 16th December 2025, the European Parliament approved a provisional agreement aimed at streamlining and reducing the scope of corporate sustainability reporting and due diligence requirements.

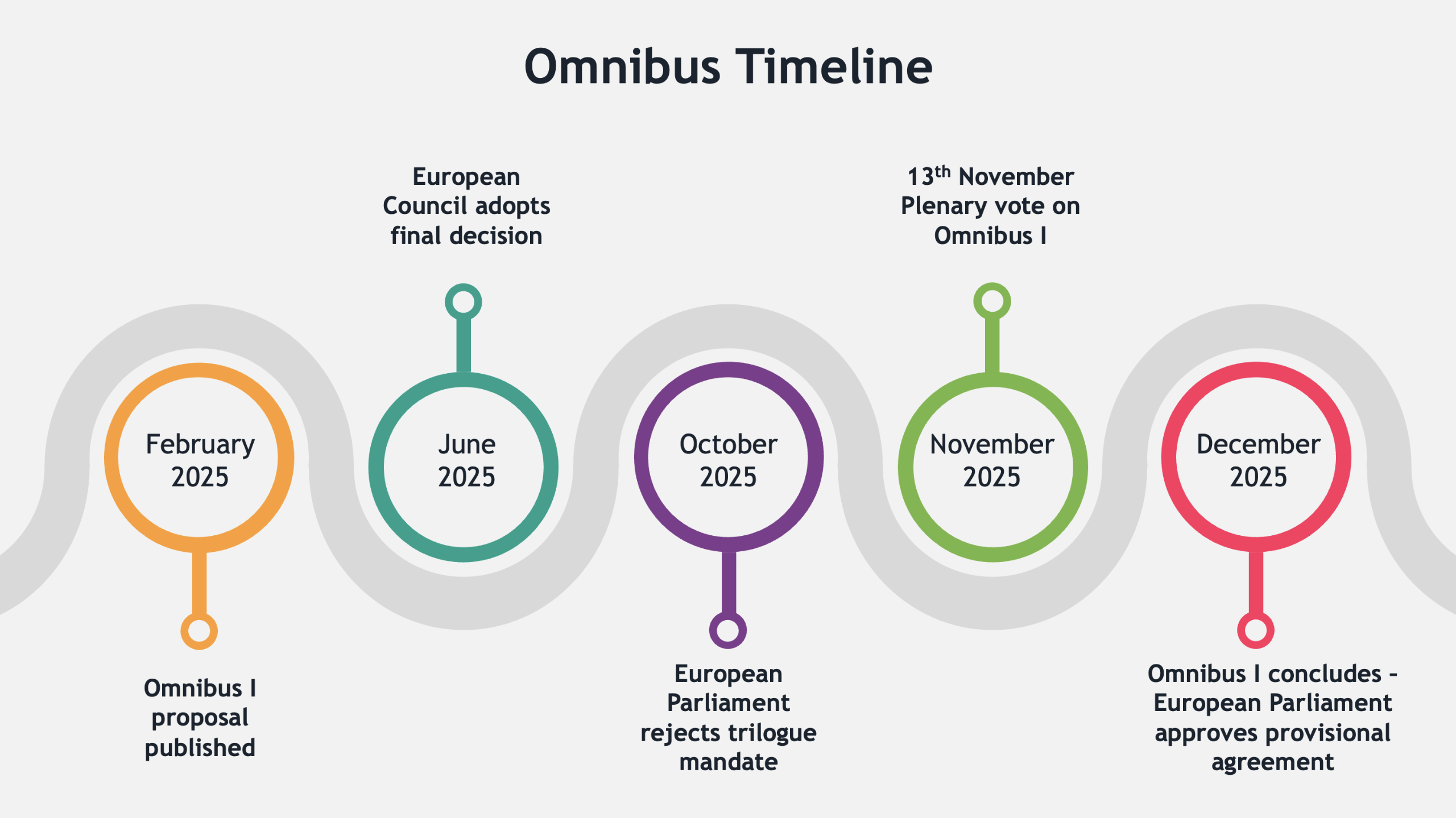

This decision finalises the ‘Omnibus I’ package, originally proposed by the European Commission in February 2025 to simplify sustainability and due diligence reporting under the Corporate Sustainability Reporting Directive (CSRD) and Corporate Sustainability Due Diligence Directive (CSDDD). Post final agreement from the European Council, a clear picture is now emerging on the requirements for corporates under CSRD and CSDDD.

The key headlines for businesses are outlined below.

Where are we now?

The first Omnibus package was published back in February 2025, and the timeline below highlights the key milestones in the development of the proposal throughout the year.

What should Irish businesses focus on now?

VSME: Why this matters more than ever?

Developed by EFRAG, the Voluntary SME Standard (“VSME”) offers SMEs a simplified, more proportional way to disclose sustainability information. Under the Omnibus agreement, VSME becomes even more significant as the EU shifts towards reduced CSRD thresholds. For many Irish SME’s that fall into the value chain of larger CSRD reporters, the VSME can serve as a practical and standard way to provide ESG information.

Companies can choose either a Basic or a Comprehensive module, proportionate to their business needs. The Basic module focuses on a smaller set of data points that offer a higher level of disclosures. It is helpful for companies with limited resources or those that respond to less burdensome value chain requests. The Comprehensive module builds on the Basic module and is more closely aligned with ESRS metrics.

These modules give SME’s flexibility while ensuring disclosures remain consistent. Furthermore, EFRAG’s VSME Digital Template and XBRL Taxonomy offer a structured, digital approach to reporting sustainability information in a standardised and accessible format. It facilitates easier regulatory compliance and improves the usability of sustainability data for stakeholders.

Source: EFRAG VSME Standard: https://www.efrag.org/sites/default/files/sites/webpublishing/SiteAssets/VSME%20Standard.pdf

What happens next?

Article written by Jennifer O'Connor, Sustainability Manager, BDO Ireland Sustainability Services.

Marc Aboud